Last weekend, anti money laundering (AML) regulations hit the headlines, following reports that big U.S. banks enable large transactions for the very people that AML rules are meant to stop. Yes, that’s unquestionably bad. But the point that’s missed is not just that AML is failing but the lack of effort to objectively measure whether AML is effective. The fact that a tiny fraction of 1% of criminal proceeds is seized says it’s not working. That’s despite the enormous economic cost borne by SMEs and those financially excluded because of AML. Not to mention the privacy invasion of ordinary people and the Orwellian Big Brother role delegated to banks.

Preventing money laundering is a worthy cause, but if it’s not working, fix it fast or find another away. Don’t allow decades more of economic cost with little gain. Ledger Insights started to explore the topic before last weekend’s news, and we were surprised at the lack of measurement of effectiveness given its negative impact.

Measuring AML’s impact is certainly not easy. But we believe it might be possible.

There is surprisingly little academic research on the subject. In part because of a lack of good data.

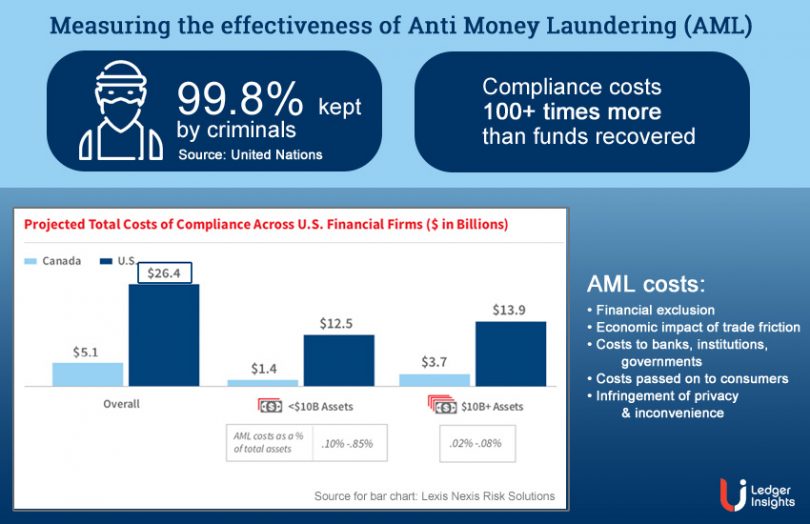

Ronald F. Pol of Australia’s La Trobe Law School has focused on the topic in the last few years. He assesses the impact of anti money laundering (AML) on crime is more like a twentieth of 1%. Or 99.95% of criminal proceeds get through. United Nations statistics based on 2009 data put the figure at around 99.8%.

In a paper published in the Journal of Policy Design and Practice Pol writes: “anti-money laundering policy intervention has less than 0.1 percent impact on criminal finances, compliance costs exceed recovered criminal funds more than a hundred times over, and banks, taxpayers and ordinary citizens are penalized more than criminal enterprises.”

He added a caveat: “The data are poorly validated and methodological inconsistencies rife, so findings cannot be definitive, but there is a huge gap between policy intent and results.” Based on our research of FATF peer reviews, we have to agree.

We stumbled upon Pol’s article after reading several of the Financial Action Task Force (FATF) country reviews on AML ‘effectiveness’. FATF is the inter-government body formed more than 30 years ago to address money laundering. It provides a 196 page document on how to conduct country AML “effectiveness” reviews. We found a lack of hard data on real impact often resulted in the use of general crime statistics, anecdotal evidence and subjective conclusions.

If AML doesn’t have the impact on the bad guys in the way we’d hoped, it has the side effect of helping to provide governments with intelligence about both illegal tax evasion and legal tax avoidance.

If you’re reading this article, you’re probably interested in blockchain and innovation. And AML is one of the biggest frictions in the fintech sector. Until last year, Ripple based its entire business model on AML frictions. Its RippleNet messaging service (and JP Morgan’s IIN) helps banks to better communicate payment delays because of AML. And the XRP cryptocurrency enables transfers for remittance companies that struggle to open bank accounts because of AML restrictions. Those remittance companies are restricted because they are the ones that aid people locked out of the banking system, often also because of AML. SWIFT has received a bad rap, even though it transmits payment messages in real time. The hold up is mainly AML bank queries or institutions that sit on the money with AML as an excuse for delay.

The news

Last Sunday, BuzzFeed News and the International Consortium of Investigative Journalists published reports about money laundering, the so-called FinCEN files. These analyze 2,100 suspicious activity reports filed by banks with U.S. Treasury Department’s Financial Crimes Enforcement Network.

The ICIJ wrote: “The records show that five global banks — JPMorgan, HSBC, Standard Chartered Bank, Deutsche Bank and Bank of New York Mellon — kept profiting from powerful and dangerous players even after U.S. authorities fined these financial institutions for earlier failures to stem flows of dirty money.”

The Wall Street Journal quoted a a former Treasury sanctions official, Elizabeth Rosenberg: “The FinCEN files illustrate the alarming truth that an enormous amount of illicit money is sloshing around our financial system, and that U.S. banks play host and facilitator to rogues and criminals that represent some of America’s most insidious national security threats.”

In an excellent book that explores the topic of AML, Italian professor Maciandaro from Bocconi University outlines the societal costs of giving criminals a free pass. The book outlines how every dollar of criminal proceeds reinvested, leads to more and more crime. “Since money laundering can lead to an explosion of crime rates, it is a ticking time bomb and therefore create(s) a serious problem that has to be fought,” the book states.

The costs of AML

Arguably there are at least four costs of AML, and there should be some attempts to measure each one. They are the direct costs to banks and regulators, the economic price of friction for businesses and trade, the impact on financial inclusion, and the government’s erosion of citizen privacy. The latter may be harder to measure directly, but could indirectly lead to greater pushback on citizen compliance, as witnessed with COVID-19.

The easiest one to assess is the direct costs to banks of AML. Here Lexis Nexis Risk Solutions assessed the cost to U.S. banks as $26.4 billion annually. We’ll come back to the “yield” from that expense. But a hint is that total federal asset forfeitures for 2019 per the Department of Justice was $2.2 billion. Most is unrelated to AML efforts.

There are also the bank costs passed on to businesses and consumers as a result of AML, which should be capable of measurement.

Then there’s the economic cost of friction. “The requirements to merely participate in trade are typically too onerous for most SMEs to trade safely and/or efficiently,” notes the OECD. “Challenges with unintended consequences of financial regulation have been highlighted by Business at OECD and the B20 for several years.”

And it goes on: “The typical cost-to-income ratio in traditional trade finance is 50-60%, meaning that more than half of the price charged to clients for trade is used to cover operational expenses, even before covering the costs of risk, liquidity and capital.” Now that’s not entirely AML, but as can be seen from the Lexis Nexis figures, AML costs are not a minor component.

The OECD and G20 business advisory group B20 have launched plans to use blockchain to help SMEs with financial compliance burdens by issuing a GVC Passport identity for businesses.

Turning to financial inclusion, the impact of AML was not just predictable but predicted by the World Bank back in 2006. “The introduction of new or tightened AML/CFT regulations may have the unintended consequence of reducing the access of low-income people to formal financial services,” wrote the World Bank. “Besides the additional costs of compliance to financial service providers, standard customer due diligence rules may be difficult to apply for typical microfinance clients, especially in countries that have weak national identification systems. “

And finally, we’re sleep walking into a whole new league of privacy invasion. To date, it has generally been transactions of more than $10,000 that get reviewed. But if digital currency becomes mainstream, then the FATF virtual asset rules bring that down to $1,000. And the sharing of your personal data is with many more nonbank financial institutions. For some, digitally paying rent will be a reportable event. Also, these figures rarely move with inflation, so the degree of oversight increases. $10,000 in 2000 is equivalent to $15,000 today.

Many know your customer (KYC) identity sharing initiatives are well-intentioned to reduce the paperwork burden on consumers and businesses. But some of the digital solutions may result in people sharing more data than they otherwise might want to, sometimes without realizing how much data they’re passing on.

We’ve briefly explored some of the costs. So how do we assess the benefits?

Measuring the impact of AML

The ultimate measure of AML is the amount of criminal proceeds confiscated as a direct result of AML.

Returning to the research by Pol, he notes: “FATF blames governments for ‘taking a tick-box approach to regulatory compliance, and focusing on processes rather than outcomes’, seemingly oblivious to public policy issues such as whether the design or implementation of its policy model contributes to (or causes) such behaviors.”

Because details on anti-money laundering effectiveness seemed to be hard to find, we explored FATF publications. Countries are mutually reviewed to see how they perform at AML. But the bulk of the review process focuses on the technical implementation of AML procedures.

One measure – not even close to the top of the FATF list – was amounts confiscated. But some of the data used for this ‘measure’ can be attributed to a country’s general crime statistics, not to AML.

The work involved in implementing AML globally is enormous. It seems like a relatively small effort to request banks to measure confiscation and seizures and to mark which have an AML connection. Ledger Insights asked FATF whether this has been considered but didn’t receive a response before publication. Post publication it provided an 80-page FATF guidance document on statistics which recommends governments collate the sort of data we were keen to see but were not in the reports we looked at.

Demonstrating the lack of measurement

Given we know the cost to banks in the U.S. is $26 billion annually, we thought we could go to the FATF report for the U.S. and compare that to the amounts confiscated. The review says the U.S. is rated as having a substantial level of effectiveness for confiscation.

The FATF review provided data for all federal confiscations and seizures in 2014. This amounted to $4.2 billion seized and $4.4 billion confiscated. The seized figure included two large amounts of $1.7 billion relating to the Bernie Madoff affair and $1.2 billion paid by Toyota to avoid prosecution for car safety issues. Should these count in an AML effectiveness measure?

In 2018, a different group reviewed UK AML processes. In the four years between 2014 and 2017, the UK restrained £1.3 billion ($1.65bn) and recovered £1 billion ($1.27bn). The methodology was “using POCA, civil recovery, and agency-specific disgorgement mechanisms.”

We believe this figure includes all monies recovered from any criminal activity in the UK. You know, unrelated to AML, the police do work resulting in a criminal conviction, and then an application is made to recover the funds under the Proceeds of a Crime Act Powers (POCA). The POCA figures are publicly available and given we believe these are what’s included in the FATF report, the proportion that relates to AML is unknown.

The report also mentions that the tax department HMRC recovered £3.4 billion ($4.3bn) since 2016. We suspect this is organized crime investigations that may or may not be linked to AML. It’s part of that handy side effect of AML increasing tax yield.

Turning to Switzerland, which had its FATF review in 2016, for the five years to 2015, it shows CHF 1.55 billion ($1.67bn) confiscated. That’s a rate of CHF 309 million ($332m) annually. On a positive note, as of February 2016, Switzerland had seized assets of CHF 5.8 billion ($6.2bn).

To put those figures in context, Switzerland’s banks have CHF 6.9 trillion ($7.4tn) in assets under management, of which 47.5% is from foreign clients.

An AML profit and loss account

AML needs its own profit and loss account. On the profit side is criminal proceeds confiscated or seized as a result of AML. Criminal forfeitures unrelated to AML should not be counted. Given it’s the banks implementing the seizures, this should be measurable.

On the cost side is the price of implementing AML for banks, institutions and governments, and the costs passed on to consumers. It should include the economic impact on trade, at the very least, the trade finance gap, and the cost of financial exclusion. Then there’s privacy, which is harder to measure, and as with financial exclusion, perhaps priceless.

This article isn’t trying to say that measuring the impact of AML is easy. It’s not, and FATF has its work cut out. However, it looks possible. And it’s likely significantly simpler than the global spaghetti of regulations implementing AML. Where there’s a will, there’s a way.

Update: Added a link the FATF statistics guidance