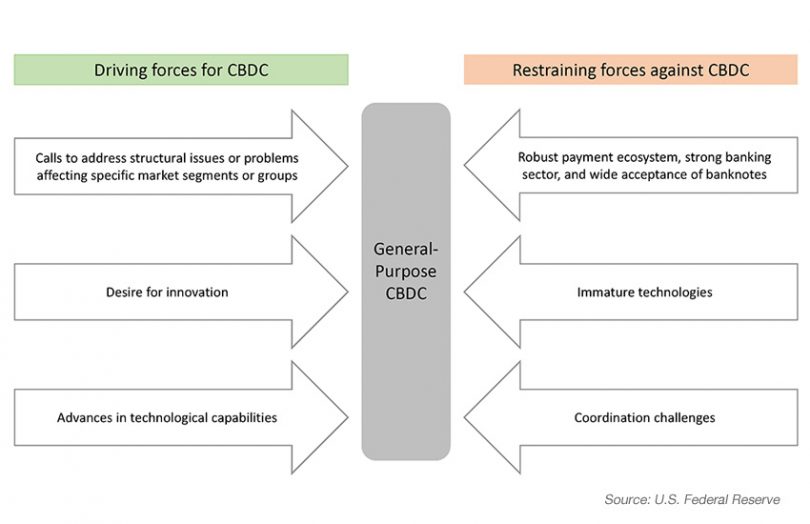

Yesterday U.S. Federal Reserve Chair Jerome Powell said of the digital dollar, “This is going to be an important year. This is going to be the year in which we engage with the public pretty actively.” He was responding to a question from Republican Representative Patrick McHenry during a congressional hearing of the House Committee on Financial Services. The Federal Reserve published a paper exploring preconditions for a retail central bank digital currency (CBDC) the same day.

Powell noted that there are tradeoffs in terms of policy and technical issues. “There are very challenging questions, so we want to have a public dialogue about that,” said Powell. In the meantime, the Federal Reserve is exploring technical challenges and collaborating with other central banks.

McHenry said, “I think the project’s vital. I think it’s vital for American competitiveness. But also there’s a fear that some want to use the digital dollar as a way to kill private sector innovation and our banking system.”

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.