On Twitter earlier this month, Finnish central banker Aleksi Grym asked the excellent question, “Is there any difference between stablecoins and e-money?”

E-money is a legal concept in many jurisdictions such as Europe and Singapore, but not in the United States. And Europe wants to regulate stablecoins as e-money, which could reduce the current functionality of stablecoins, such as the ability to earn interest.

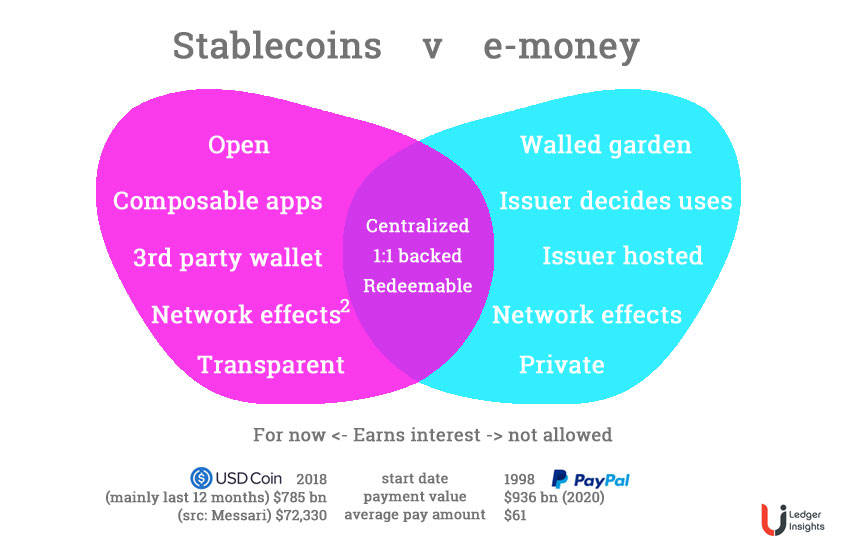

Here the stablecoin focus is on 1-to-1 fiat-backed, such as Tether, USDC and the planned Diem USD.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.