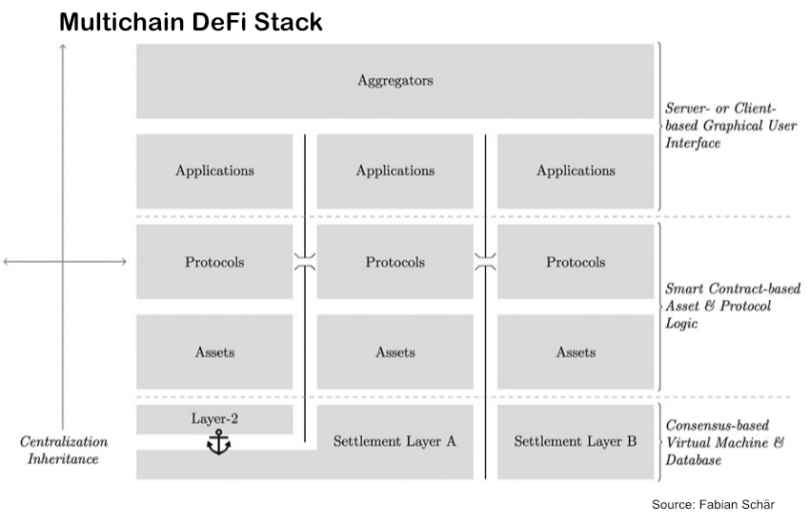

A recent academic paper on the potential regulation of decentralized finance (DeFi) goes substantially deeper than those before it. One of the authors, Fabian Schär, penned a 2021 DeFi paper that separated DeFi into functional layers. The paper focuses on these layers in search of centralization. What’s refreshing is that despite the authors being fans of DeFi, their centralization assessment is clear and intellectually honest.

They conclude that “most of what is commonly referred to as DeFi have severe centralization vectors.”

In most cases regulators use the principle of ‘same activity, same risk, same rules’ to assess who to regulate. The “who” is based on identifying individuals or organizations involved in centralized activities.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.