The protection gap

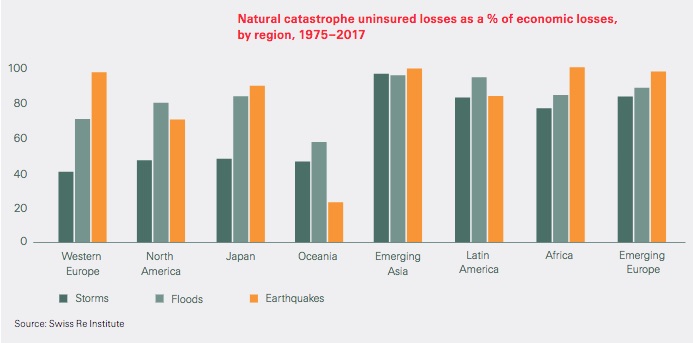

According to Swiss Re Institute in the last ten years, only 30% of catastrophe losses were insured. That means 70% ($1.3 trillion) is not covered and those losses are borne by individuals, business, and governments.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.

Image Copyright: dimol / 123RF Stock Photo