In a companion article we explored why the settlement asset question matters for tokenized securities. Stablecoins are the pragmatic default for on chain settlement, but they carry issuer credit risk, uncertain legal finality and weaken central bank monetary policy transmission. As on chain volumes grow, there needs to be optionality beyond stablecoins.

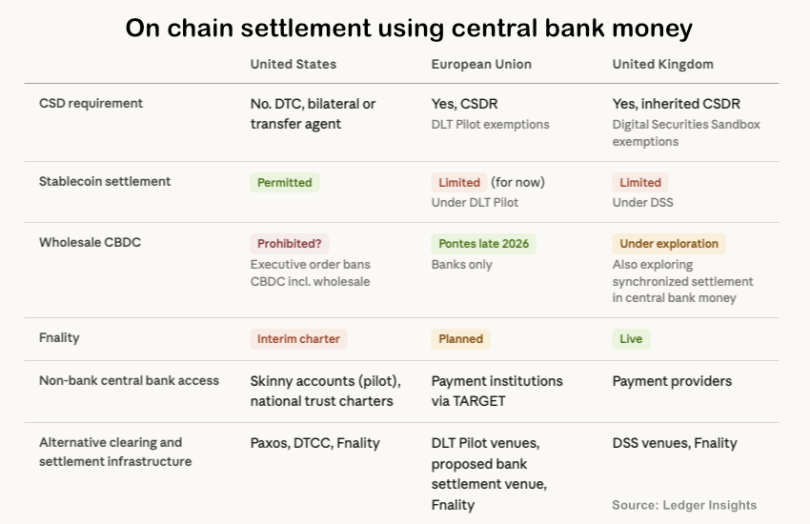

The case for central bank money anchored settlement is clear. But the practical question is how non bank institutions such as market makers and broker dealers get access to it. The answer depends on jurisdiction, but the menu of options is converging around a few models.

One reason on chain settlement matters is programmability. Smart contracts can automate complex settlement logic, enable 24/7 operations and improve collateral management. Additionally, when the settlement asset itself is on chain, delivery versus payment can be executed atomically. But these benefits are strongest with direct access. If central bank money access is intermediated through a bank, settlement involves chaining triggers together, adding latency and complexity. Given the goal of distributed ledgers is to reduce friction, why add it back? That tradeoff between direct access and intermediated access runs through every pathway discussed below.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.