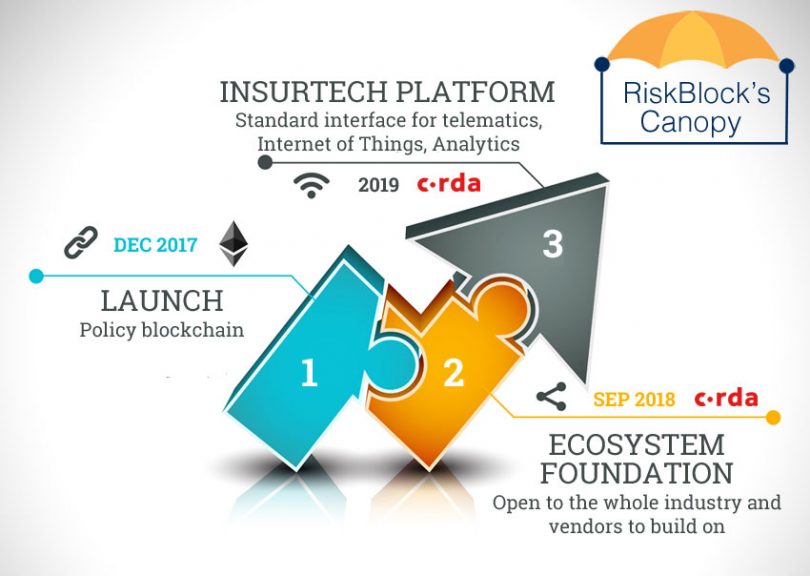

RiskBlock the insurance industry alliance, has ambitious plans for an open ecosystem for the whole

insurance sector. Later this summer they plan to launch the second version of their Canopy blockchain system to enable third parties to connect into their network and build applications on top.

While the vision is big, so is the financial potential. One application to be released later this year could save up to $300m annually in the US.

Today The Institutes RiskBlock Alliance boasts 28 members, including most of the biggest names in insurance in the US such as State Farm, Liberty Mutual, GEICO, Nationwide, USAA, Chubb, and Travelers.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.

Image Copyright: Composite: Ledger Insights, Arrow graphic: grki / DepositPhotos