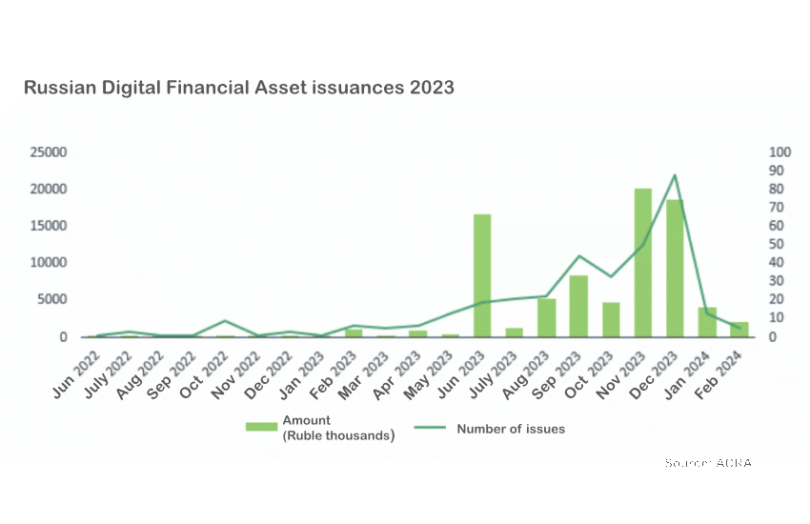

In 2021 Russia passed legislation supporting the tokenization of real world assets (RWA), calling them digital financial assets (DFA). It took a while for the central bank to authorize issuing platforms, with a trickle of issues in 2022 (perhaps three). However, in 2023 it started to take off with ten licensed entities. A recent report by rating agency ACRA estimates there were 350 issues in 2023, with an outstanding balance of around 60 billion rubles ($651 million). Russia’s largest bank Sber said it issued more than 30 DFAs by mid-2023.

“It is difficult to recall any financial instrument in the last ten or fifteen years that has shown similar growth rates in such a short period of time,” ACRA wrote. That’s despite significant restrictions on which asset classes can be tokenized and which investors can participate.

We believe that currently investors are mainly restricted to corporates and wealthy individuals. Other consumers can invest but only in certain types of assets and they have monetary limits. Institutional investors are excluded.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.