Today the U.K.’s Financial Conduct Authority (FCA)

says it proposes to ban the sale of crypto derivatives and crypto related exchange traded notes (ETNs) to retail consumers. We have three questions: Is the derivatives ban just the start? Some new blockchain technologies are derivatives themselves, could they face bans? Is it time to bring the definition of a retail investor and sophisticated investor into the digital age?

The FCA cites the reasons for the proposed ban as the nature of the crypto assets and their volatility, the risks of cyber theft and other crimes and inadequate understanding by consumers. It estimates the ban will reduce consumer losses by £75m and £234.3m.

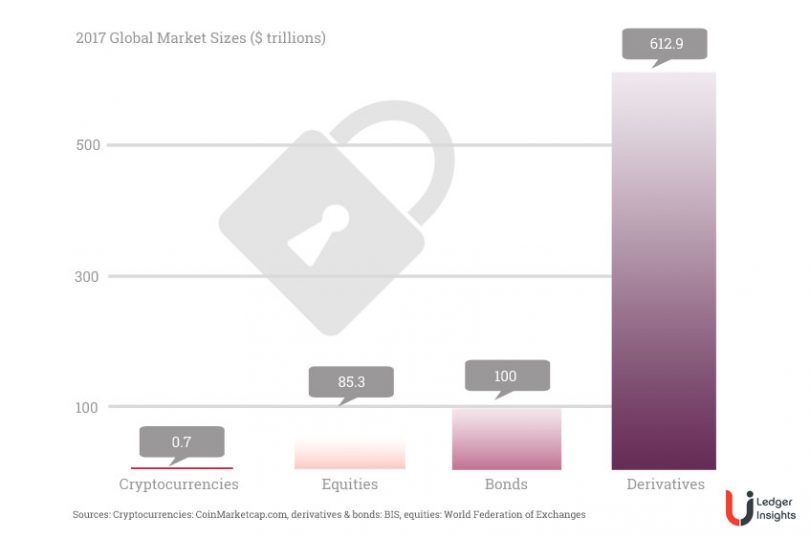

While the market at the moment may be small, the graph above shows how derivatives have a habit of dwarfing their underlying markets.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.

Image Copyright: Composite: Ledger Insights