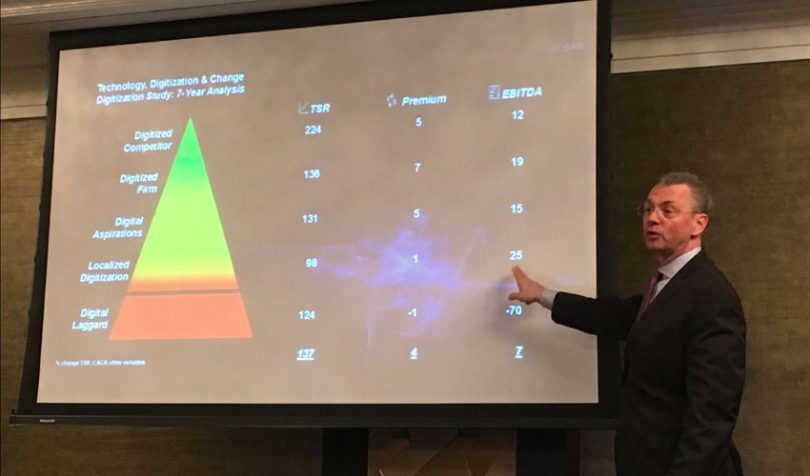

Talking at the

Blockchain for Insurance Summit, Bill Pieroni, ACORD’s CEO, spoke about the dangers of a wait-and-see approach with blockchain. The global standards-setting body for the insurance industry studied technology penetration for a hundred historical innovations including TV.

Surprisingly, they found that the rate of adoption is not much faster at roughly four percent a year. What’s changed is the lag between the initial invention and take off. In the past, it’s taken decades before the adoption takes off. However, no longer.

“You don’t have the time anymore. None of us do because by the time you figure out that it’s either dead (client-server technology) or taking off (IoT, blockchain, the rest of it). You don’t know. And you’ll never catch up because it’s not about throwing money at it,” said Pieroni.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.