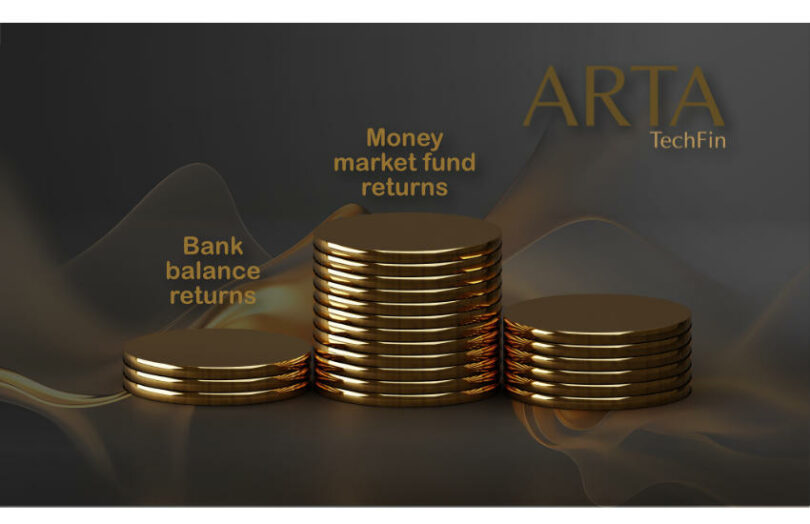

While Hong Kong is about to start the second phase of its eHKD retail central bank digital currency (CBDC) trials, last week Arta TechFin published a report on a first phase pilot. It demonstrated a very practical use of programmability. Today consumers don’t get a decent return on their small cash balances held at banks. We’ve seen crypto protocols and asset managers starting to offer tokenized money market funds. However, these are still fringe investments. The Arta pilot explores converting cash balances to a CBDC (or stablecoin or tokenized deposit) and automating the subscription to a money market fund.

This use case resembles some of Brazil’s DREX CBDC pilots, which aim to bring financial inclusion to the masses.

Hong Kong has not decided whether to issue a retail CBDC but recently commenced wholesale CBDC trials to support tokenized deposits. It also launched a stablecoin sandbox.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.