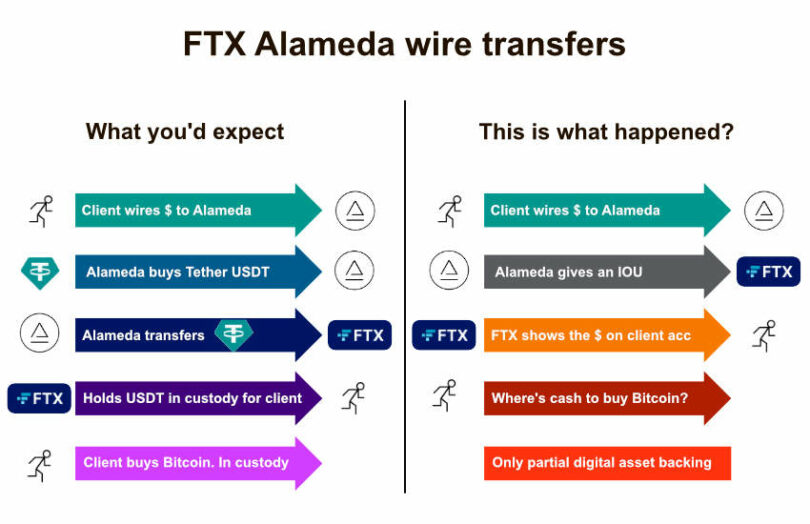

Last week Bloomberg reported that prosecutors are investigating potential fraud relating to FTX transfers to the Bahamas, presumably the ones made shortly before the bankruptcy. However, there are unanswered fundamental questions about the early days of FTX, when clients wired money to FTX via Alameda.

Former FTX CEO Sam Bankman Fried (SBF) stated that FTX lacked a bank account in the early days, so customers wired money to Alameda. And these transfers account for a significant amount of the funds owed by Alameda to FTX at bankruptcy.

This raises two related questions:

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.