Facebook has confirmed that it currently has no plans to launch its Calibra wallet in India, according to

Bloomberg. That’s because of India’s regulatory stance on cryptocurrencies. Last month India’s

Economic Times reported that there’s draft legislation entitled “Banning of Cryptocurrency and Regulation of Official Digital Currency Bill.”

In its current form, the yet-to-be-published Bill makes cryptocurrency illegal and holding crypto a non-bailable offence. There’s even a proposed ten-year prison sentence for those who “mine, generate, hold, sell, transfer, dispose, issue or deal in cryptocurrencies”.

By adopting an aggressive stance, the government hopes to prevent money laundering. Given the Bill has support from the tax and customs departments, it appears the government is keen to address digital black market trading.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.

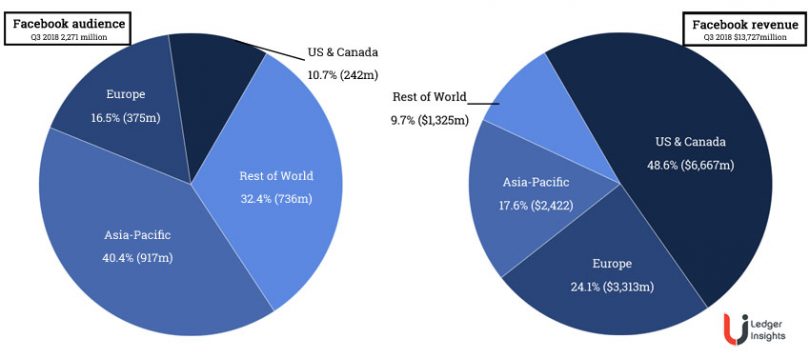

Image Copyright: Data: Facebook Graphs: Ledger Insights