This is an opinion piece by Michael Chapman, CEO of Nuvanté Technologies, a startup planning to enable the clearing of stablecoin transactions using central bank money for settlement. It’s participating in the Synchronisation Lab.

As digital assets and programmable money move from experimentation toward broader adoption, a fundamental challenge remains: how to safely settle digital transactions when the cash leg continues to rely on traditional payment infrastructure.

The Bank of England’s Synchronisation Lab is intended to address that challenge directly. The initiative explores how central bank money can support the next-generation of digital payment and settlement systems, ensuring that innovation in digital finance remains compatible with the safety and stability of existing financial market infrastructure.

The Lab forms part of the Bank’s wider programme to modernise the UK’s Real-Time Gross Settlement (RTGS) service. Its focus is on testing how different ledgers, including blockchain-based asset platforms and the Bank’s RTGS system, can be synchronised so that cash and assets move together atomically, eliminating settlement risk.

In practical terms, the Lab examines how delivery-versus-payment (DvP) and payment-versus-payment (PvP) transactions can occur simultaneously in real time. By synchronising the movement of assets and payments across different systems, this approach removes timing mismatches, reconciliation breaks and counterparty exposure that can arise when transactions settle across separate infrastructures.

Why synchronisation matters for digital payments and stablecoins

Today, many digital asset transactions settle the asset leg instantly on blockchain networks, while the corresponding cash leg settles hours or even days later through conventional banking infrastructure. This disconnect introduces credit risk, operational complexity and liquidity inefficiencies.

For emerging payment instruments such as stablecoins and tokenised deposits, the issue is even more fundamental. Without robust settlement infrastructure, digital money risks fragmenting across multiple private networks, potentially undermining the long-standing principle of the singleness of money, that different forms of money remain interchangeable at par.

The Synchronisation Lab explores a model in which conditional payment instructions in RTGS are linked to events on external ledgers. Settlement completes only when all predefined conditions are met; otherwise, both legs of the transaction safely revert.

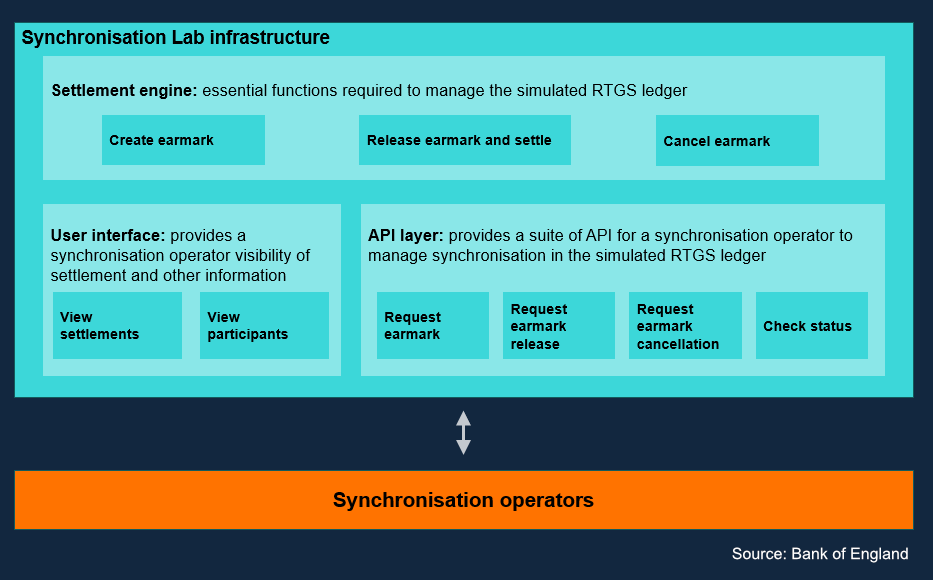

Illustrative set up of the Synchronisation Lab:

Anchoring this process in central bank money delivers settlement finality while avoiding reliance on commercial bank credit with synchronisation operators connecting the different parties and orchestrating the movements in cash and assets. The approach has the potential to support risk-free clearing for stablecoins, tokenised deposits and tokenised securities without fragmenting liquidity across parallel systems.

Industry participation and market engagement

Among the synchronisation operators participating in the Lab is Nuvanté Technologies Ltd, a UK-based financial market infrastructure developer focused on clearing and settlement infrastructure for digital money and tokenised assets. Through the Synchronisation Lab, Nuvanté is exploring the practical implementation of atomic settlement for stablecoins and delivery-versus-payment settlement for tokenised securities, with settlement in central bank money.

“The real challenge for digital money isn’t issuance, but safe settlement. Anchoring settlement in central bank money would allow digital assets, including stablecoins, to interact without introducing additional settlement risk.”

Internationally, other central banks are also examining how payment infrastructure may need to evolve alongside digital asset markets. In the United States, for example, the Federal Reserve, recently requested public input on a proposed payment account for eligible institutions for the limited purpose of clearing and settling payments. The consultation closed on 6 February 2026, reflecting growing central bank engagement with the future design of digital financial infrastructure.

RTGS and the move to RT2

At the centre of this transformation is the Bank of England’s renewed RTGS service, often referred to as RT2. RT2 introduces a modern, API-enabled architecture alongside enhanced messaging standards, including ISO 20022. These upgrades enable richer data exchange and more flexible interaction with the RTGS system.

The new platform is designed to support event-driven payment flows and conditional settlement logic, capabilities that are essential for synchronised settlement with external ledgers.

By enabling conditional payments and real-time feedback between systems, RT2 provides the technical foundation for the atomic settlement models being tested in the Synchronisation Lab. Over time, this could allow digital payments and tokenised markets to settle safely in central bank money without reintroducing settlement risk through intermediaries.

Looking ahead

The innovations emerging from the Bank of England’s Synchronisation Lab represent an important step in bridging the gap between digital innovation and trusted monetary infrastructure.

As stablecoins, tokenised deposits and digital securities move toward regulated adoption, the ability to settle transactions safely will be critical. Synchronised settlement offers a pathway to integrate new forms of digital finance into the financial system while preserving the safety, finality and trust that underpin modern markets.

If successful, the Synchronisation Lab could help shape how central banks worldwide connect their payment systems with emerging digital asset markets in the years to come.