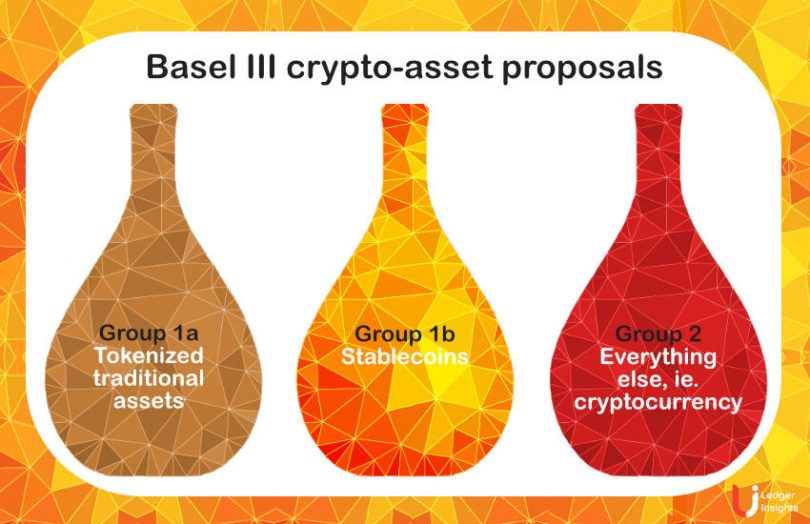

The second crypto-asset consultation by the Basel Committee for Banking Supervision closed at the end of September and it published the feedback received. One of the proposed rules limits the amount of bank cryptocurrency exposures to 1% of Tier 1 bank capital. Some of the feedback concluded that means that most of the world’s largest banks can have a combined $20 billion exposure to crypto-assets.

Update: the final rules have now been announced.

There’s a lot of detail in the proposed Basel rules, but the four most significant issues are:

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.