Cambridge Centre of Alternative Finance (CCAF) released its second

Global Enterprise Blockchain Benchmarking Study.

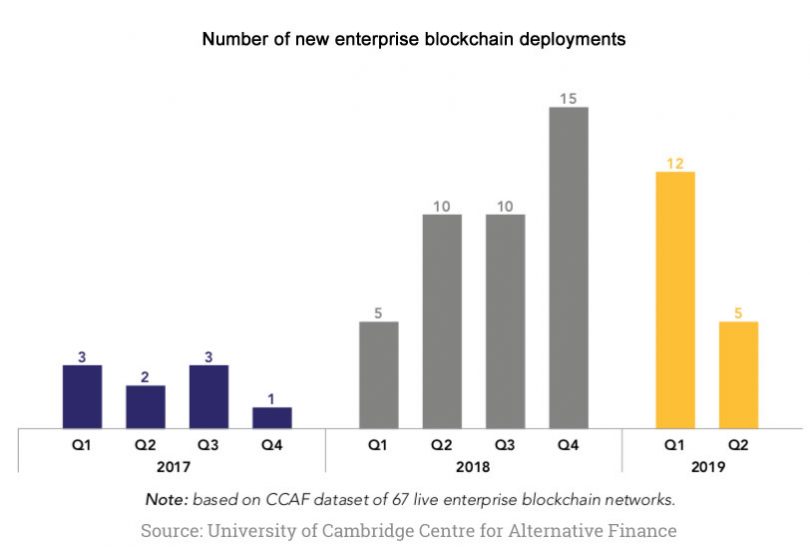

CCAF talked to more than 160 respondents and observed 67 live networks. The paper notes that a lot of the hype surrounding distributed ledger technology (DLT) has faded and corporates are considering more realistic approaches. Keith Bear, IBM’s former VP of Financial Markets (until Jan 2019) is a co-author of the report.

Networks founded by single entities rather than consortium

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.