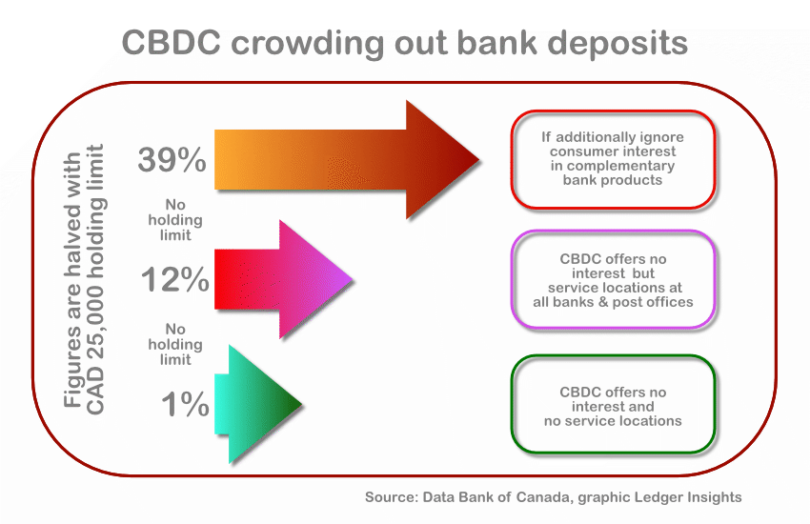

Economists at the Bank of Canada ran a model to assess the impact of introducing a retail central bank digital currency (CBDC) on bank deposits. It’s widely expected that a proportion of bank deposits will switch to a CBDC. The economists believe that most assessments neglect the fact that banks provide products that complement deposits, such as mortgages and credit cards. If you assume consumers don’t care about the other products their bank offers, then 39% of deposits could be crowded out by CBDC.

However, CBDCs are not perfect substitutes for bank deposits. So, if you consider consumer affinity for other bank products, the Canadian model estimates that just 12% of deposits would switch to CBDC. They based their data on a 2010-2017 household survey. It showed 56% of deposit holders had a mortgage from the same bank, and 45% had a bank credit card. The study assumes the CBDC does not offer interest.

An additional factor from the survey is consumer affinity for bank branch visits for customer service, support and complaints. Hence, they included this in the model as well. If a CBDC had no service points, they estimate the volume of deposits switching to CBDC would be just 1%. However, that wouldn’t be an ideal scenario. So, the 12% figure assumes consumers can get support for a CBDC at all banks and post offices.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.