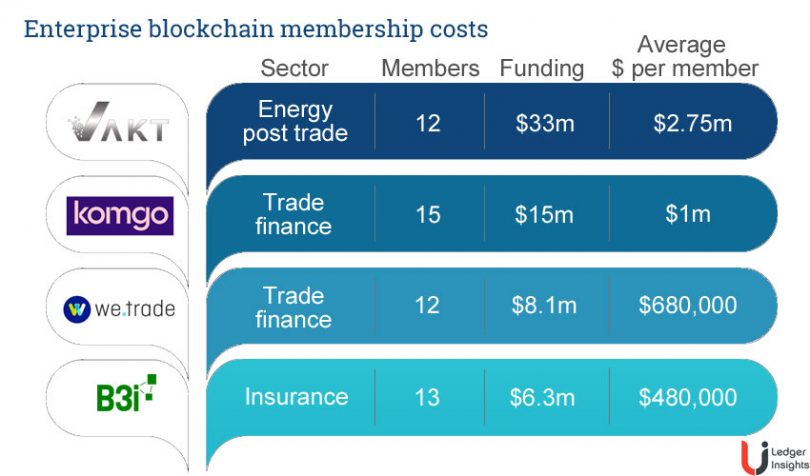

Enterprise blockchains are consortia by their nature, so the cost is spread over member investors. But spreading a large investment can still involve a significant outlay. The question is how much does it cost to join an enterprise blockchain consortium? And the obvious answer is “it depends”. We’ve uncovered the specifics of four large initiatives. The current funding for those projects ranges from $6.3m to $33m giving an average investment per member of $1.2 million.

In three out of the four, the company average investment is roughly representative of the amount paid by all shareholders, except for VAKT where the average represents a broad range from $1m to $5m. The number of shareholders for the four companies varies from 12 to 15.

With just four projects, it’s hard to claim that they’re representative of all enterprise blockchains, particularly because the two substantially better-funded projects, VAKT and komgo, have numerous energy sector investors. On the flipside, B3i the insurance initiative is likely to close its second funding round soon, and hence its figures are understated.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.

Image Copyright: Shape: khvost / BigStock Photo, composition: Ledger Insights, logos: respective rights holders