Highlights:

On Tuesday, it was announced that Facebook invested $5.7 billion to take a 9.9% stake in Indian mobile operator Reliance Jio. The company was a wholly-owned subsidiary of Reliance Industries, India’s largest company according to Fortune India. Both parties stated that the tie up was about helping small businesses with digital. This is also an aim of Facebook’s Libra payments and digital currency initiative.

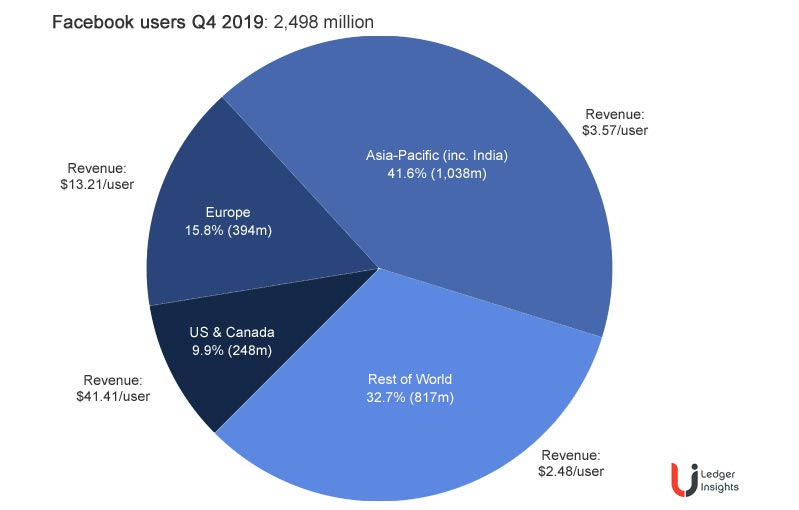

India is already the largest market for both Facebook (260 million users) and Facebook-owned WhatsApp (400 million users). But it lags significantly in terms of revenues. The revenue per user in North America at $41.41 is 11.6 times the average user revenue in the Asia-Pacific, including India. So the Jio deal is about commercialization as opposed to user acquisition.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.