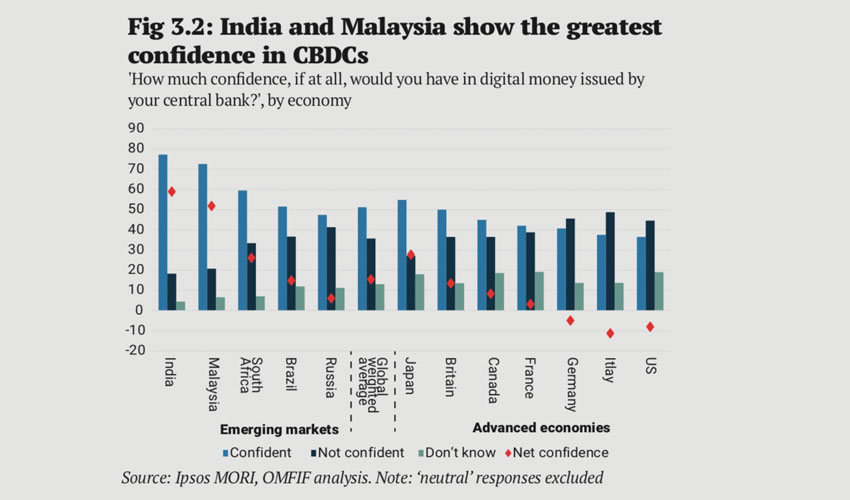

Yesterday the Wall Street Journal (WSJ) published an article about the pros and cons of a U.S. central bank digital currency (CBDC) or a digital dollar. However, recent research by MORI and OMFIF showed that U.S. citizens are not keen.

The survey found that the number of U.S. residents that have confidence in the Fed Reserve as an issuer of digital currency was less than those who are non-believers. The net figure was a negative 8%. Of the 13 countries surveyed, the only state that was more against the idea was Italy.

In the WSJ article, MIT head of the Digital Currency Initiative Neha Narula outlined the advantages of a CBDC. She pointed to the oft-quoted potential benefits of cheaper payments, both domestic and international. And the ability of the Federal Reserve to influence monetary policy.

Article continues …

Want the full story? Pro subscribers get complete articles, exclusive industry analysis, and early access to legislative updates that keep you ahead of the competition. Join the professionals who are choosing deeper insights over surface level news.